{kind=link}

We are in very interesting times today. It’s rare to see so many tectonic shifts happening in real time: High interest rates, declining equity values, SVB and other banks failing with a continued contagion risk and a recession looming.

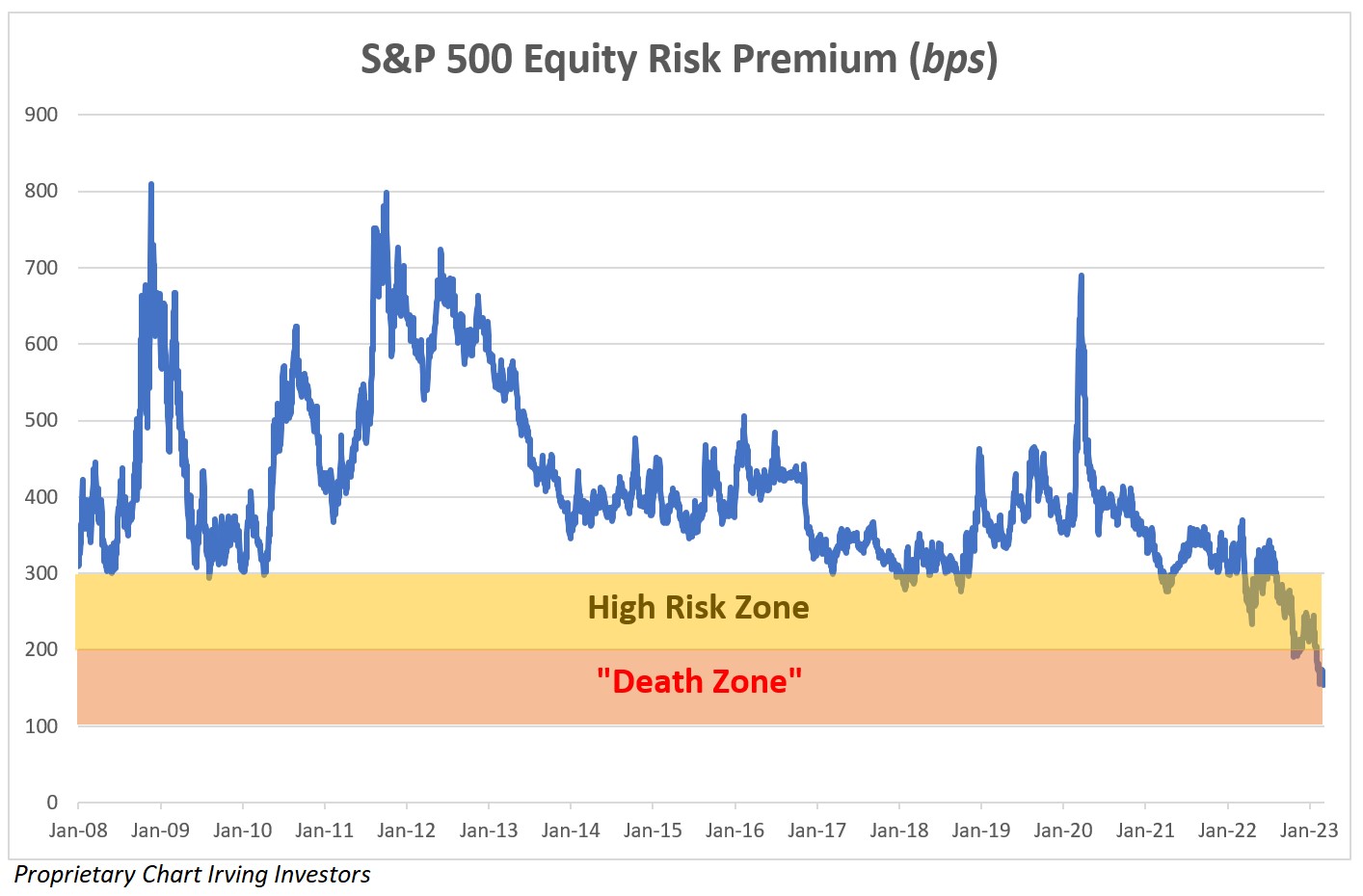

There has been an aggressive shift in assumed equity returns compared to fixed income returns. The data tells a clear and extreme story.

Simply put, equity risk premiums (ERPs) have broken down well below the ranges that were established since 2008. The ERP calculates the projected S&P returns versus the returns of 10-year treasury bills (data from Morgan Stanley).

The below chart is important to the startup audience because it speaks to why fundraising is extremely challenging right now and why valuations are coming down so dramatically. Opportunity cost is powerful indeed.

For the venture world specifically, this dynamic is compounded by the venture debt markets cooling, which in turn makes equity the most viable option for most.

Image Credits: Irving Investors

The factors at play

Waiting for a rebound in public market multiples to preserve previous valuations has not proven to be a good strategy.

Venture capital activity has declined

Deployment of VC capital continues to slow down. SVB measured the inflow and outflow of deposits by a metric called total client funds (TCF), which has been negative since the first quarter of 2022 (five straight quarters now).

This trend is continuing in 2023: VC capital deployment declined another 60%, and deal count has dropped about 25% from a year earlier.

Declining venture activity combined with dropping ERPs is a clear signal that there needs to be a material correction in private tech company valuations. However, anecdotally, we have seen that private company valuation expectations have remained lofty relative to obvious public comparables.